Read more:

https://majedaltir.com/geopolitics-in-business/

Geopolitics Is Now a Business Function: Read the Map or Lose the Market

Geopolitics Is Now a Business Function: Read the Map or Lose the Market

Geopolitics in business is no longer a peripheral concern. It has become a primary driver of corporate value, influencing strategy, investment, supply chains, and market expansion.

Why Geopolitics in Business Has Moved into the Boardroom

Geopolitics in business is now a strategic discipline rather than a political concern reserved for specialists.

Since 2016, the sequence has been relentless. Brexit fractured regulatory assumptions across Europe. The US and China entered a trade war that reshaped manufacturing geography. Russia’s 2022 invasion of Ukraine disrupted global energy and commodity markets and forced multinational corporations to write off billions in stranded assets. Attacks on shipping in the Bab el-Mandeb strait from late 2023 onward collapsed container vessel transits by roughly 70 percent and added weeks to delivery schedules. Each event linked geopolitical risk directly to profit and loss.

For organizations operating in or from Saudi Arabia and the GCC, this shift carries a dual nature. The region is exposed to global shocks in energy, logistics, and international trade. Simultaneously, it is becoming a central economic and political hub reshaping where capital, talent, and brands flow. Riyadh is no longer a downstream market. It is a node. Geopolitical risks alter the global business environment, and the GCC is now both subject to that alteration and an active force within it.

The central argument is direct: executives who cannot read the geopolitical map cannot allocate capital, design supply chain networks, or plan cross-border expansion responsibly. This article rests on three pillars. First, identifying the rise of new regional economic hubs. Second, managing risk profiles when entering markets across borders. Third, building geographically and sectorally resilient business portfolios.

From background noise to operating variable

The evolution of geopolitics in business has fundamentally changed how organizations evaluate growth opportunities and strategic risk.

Before 2010, most corporations treated geopolitical risk as a subset of legal or security work. Country risk models existed, but they served insurance and compliance functions, not investment decisions. Boards rarely discussed political instability as a direct input to product roadmaps or capital allocation.

The shift came through shock after shock:

- The Arab Spring in 2011 exposed how quickly social unrest could shut down supply routes, labor markets, and tourism demand across the Middle East and North Africa.

- Russia’s annexation of Crimea in 2014 introduced a new sanctions architecture that economic sanctions can drastically change multinational corporations’ operations, forcing firms in energy, metals, and agriculture to find alternative suppliers.

- Brexit in 2016 created immediate regulatory divergence. Companies with UK and EU operations faced new customs costs, compliance overhead, and relocation pressure.

- COVID-19 in 2020 revealed that over-reliance on single geographies for manufacturing and supply was a systemic vulnerability, not a cost advantage.

- The Russia-Ukraine conflict has disrupted global energy markets on a scale that repriced commodities globally. Over 1 billion barrels of crude were displaced due to geopolitical conflicts tied to sanctions and market exclusion.

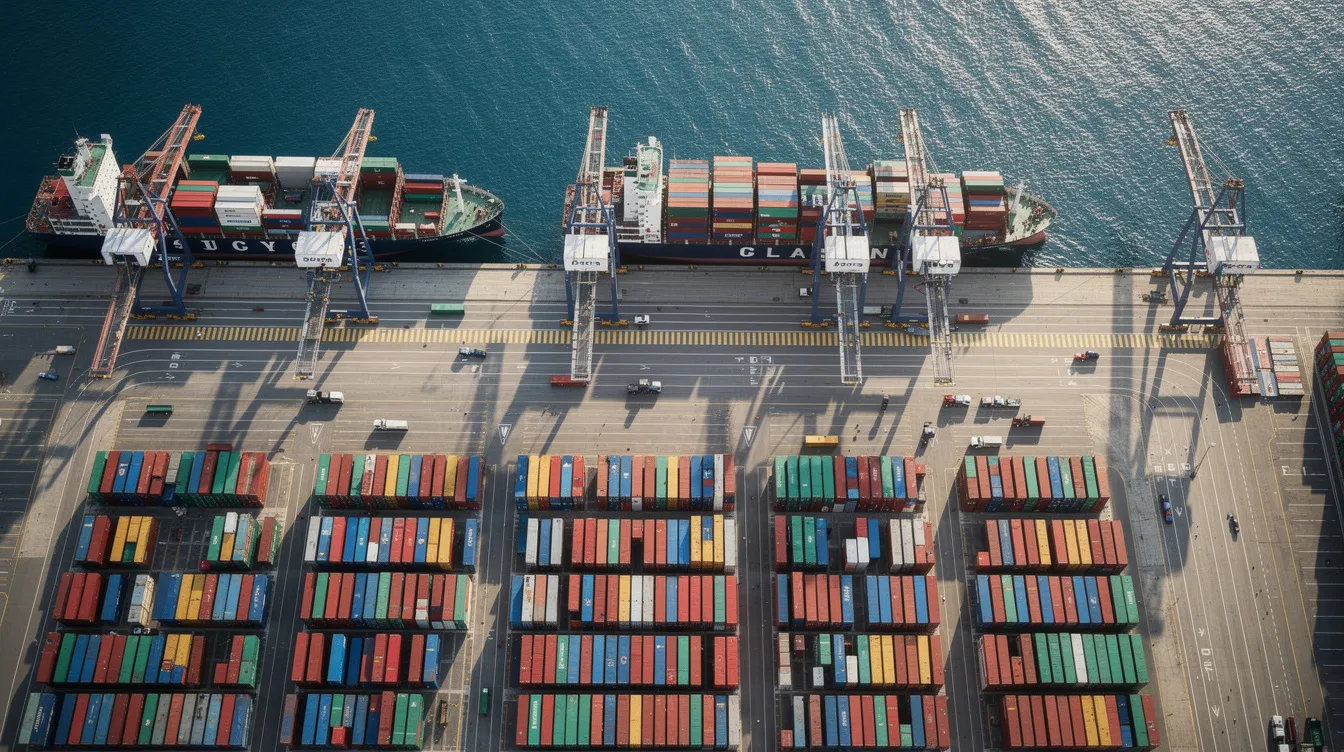

- Red Sea attacks from 2023 onward forced shipping reroutes around the Cape of Good Hope, inflating freight costs and adding 10 to 14 days of transit time on key Asia-Europe lanes.

Market volatility often increases during geopolitical tensions. Investors may turn to safe-haven assets during geopolitical crises, and geopolitical risks can lead to higher trading volumes and price swings across financial markets. Each of these shocks translated into measurable business impacts: rerouted supply chains, capital flight, regulatory changes, and abrupt market closure. Geopolitical risk management now intersects directly with corporate strategy, not as an appendix, but as a core variable.

“Strategy that ignores geopolitics is now incomplete, however elegant the spreadsheet.”

Reading the new economic map: clusters, corridors, and choke points

Understanding geopolitics in business means understanding where political alignment creates competitive advantage.

The old economic map rewarded proximity to cheap labor or raw materials. The new map rewards proximity to regulatory stability, capital access, logistics connectivity, and political alignment. Executives must now understand economic clusters, corridors, and choke points as operational coordinates, not academic concepts.

Since 2015, several emerging economic hubs have gained weight. In the GCC, Riyadh, Dubai, and Abu Dhabi are drawing multinational headquarters, sovereign capital, and talent. ASEAN nodes like Singapore and Ho Chi Minh City attract companies pursuing China-plus-one strategies. African gateways such as Nairobi and Lagos benefit from the African Continental Free Trade Area, youth demographics, and infrastructure investment. These hubs matter because they concentrate the risk factors that determine whether market entry succeeds or fails: regulatory quality, financial institutions, logistics infrastructure, and demand.

Critical choke points convert geopolitics into operational cost. The Strait of Hormuz carries roughly 20 percent of the world’s oil supply. The Bab el-Mandeb and Suez Canal corridor is the artery for Asia-Europe trade. When Red Sea disruptions forced reroutes, spot freight rates on Asia-Europe lanes jumped from approximately $3,200 to $7,500 per forty-foot container. Supply chain disruptions can arise from transportation bottlenecks and trade disputes at any of these points. Disruptions in transportation routes can delay delivery of goods by weeks. Increased shipping costs arise from rerouted logistics due to conflicts, adding $200 to $400 per container in fuel, crew costs, and war risk insurance premiums. Geopolitical tensions can disrupt global supply chains significantly, and the potential impact is no longer hypothetical.

Saudi Arabia and the GCC as a rising economic cluster

The GCC is transforming from a regional oil rent zone into a contiguous cluster of diversified economic power, with Saudi Arabia at its center. Several forces are driving this:

- Vision 2030 has introduced regulatory liberalization for foreign investment, relaxed ownership rules, and created special economic zones. This signals to global investors that the risk-reward calculus in the region is shifting materially, and emerging market opportunities arise from geopolitical change and diversification.

- Riyadh’s prime office market reflects the momentum. Rents jumped 23 percent and vacancy rates dropped to roughly 2 percent as multinational corporations established regional headquarters. King Abdullah Financial District now hosts over 140 office tenants and more than 75 regional headquarters.

- GCC sovereign wealth funds reached approximately $15 trillion in assets under management in 2025, deploying around $66 billion into AI and digital sectors. These are not passive investors. They lead controlling stakes and shape technology ecosystems.

- Giga-projects such as NEOM, Qiddiya, and Diriyah create multiplier effects across construction, hospitality, digital services, and cultural industries, generating demand that draws global supply and services into the region.

- The UAE ranks in the top 20 for ease of business, reinforcing the GCC’s collective regulatory competitiveness.

- Global organizations now treat the GCC not as a single market but as a base portfolio for wider Middle East, Africa, and South Asia strategies. Geographic location, visa liberalization, and cross-border logistics connect the cluster to the MENA region, Indian Ocean trade, and East African growth corridors.

The implications for boards are clear: decisions taken in Riyadh or Abu Dhabi increasingly shape regulatory conditions, investment flows, and economic growth across the broader region.

Geopolitics in Business and Corporate Strategy: from slide to system

Most corporate strategy decks treat geopolitical risk as a late-stage appendix, a colored heat map shown after the financial model is already built. That sequence is backwards. Embedding geopolitical analysis into corporate governance is becoming essential because the global economy is no longer a single integrated system. Business leaders must navigate a fragmented global economy influenced by policy, where governments impose tariffs and investment restrictions affecting market access without warning.

Three concrete levers pull geopolitics into the center of corporate strategy:

- Portfolio design: map every existing and prospective geography for exposure to sanctions, conflict, and regulatory reversal. Companies increasingly treat natural resources and technology as strategic assets, and portfolio logic must reflect that.

- Capital allocation timing: delay or accelerate investment based on political calendars, election cycles, and treaty negotiations. The US-China trade war from 2022 to 2025 caused stock-market losses of 17 to 42 percent for affected firms before the truce. Political changes create regulatory uncertainties that increase compliance costs and can strand investments.

- Pathway selection: choosing between joint venture, greenfield, or acquisition must account for local laws, applicable laws, regulatory predictability, and alignment with sovereign economic visions.

Geopolitical tensions can lead to increased operational costs for businesses that fail to integrate these levers. Fintech companies face sanctions exposure and data sovereignty rules. Heavy industry faces energy supply risk and transportation chokepoints. Competitor analysis must now include which political blocs your rivals are aligned with, not only their pricing. Geopolitical risk management should sit alongside financial modeling, not beneath it.

Managing geopolitical risk in cross-border market entry

For executives, geopolitics in business has become a core requirement before entering new markets.

Market entry in an era of geopolitical uncertainty requires careful consideration of risk factors that extend far beyond commercial demand. Market entry risks include internal, external, and legal factors. Companies may face expropriation in politically unstable regions. Cultural differences can impact product reception in new markets. The businesses that succeed are those that treat political risk analysis as a prerequisite, not an afterthought.

Practical tools executives should insist on before committing capital:

- Political risk analysis and country risk benchmarking that evaluate political stability, regulatory landscapes, and the financial situation of sovereign counterparties. Research from bodies like the World Bank provides baseline data, but effective assessments analyze political stability and regulatory landscapes at a granular level.

- Stakeholder mapping that identifies regulators, government ministries, and community actors whose foreign policy positions or domestic agendas could support or block entry.

- Scenario planning that must evaluate multiple plausible geopolitical scenarios, including trade war escalation, conflict spillover, and regime transitions across relevant time periods.

Companies that analyze geopolitical risks improve resilience and identify opportunities. Geopolitical risk assessment helps businesses anticipate political threats before they materialize. Companies often partner with advisory firms to evaluate risk exposure across countries with divergent trade policies.

Real-world cases illustrate the stakes. US-China trade tensions redirected manufacturing to Vietnam, India, and Mexico, reducing U.S. imports from China by roughly 25 percent. European companies divested from Russia after 2022 because of sanctions exposure and payment risks. In the GCC context, market entry now means engaging with sovereign strategies like Vision 2030 and national industrial policies, understanding Saudization requirements, and aligning with localization mandates. Businesses encounter a regulatory environment that rewards long-term commitment over short-term extraction.

“Reading the map has become an operational skill, not a specialist hobby.”

Supply chains under pressure: redesigning for geopolitical resilience

Geopolitics in business now shapes supply chain design more than cost optimization alone.

COVID-19 exposed over-reliance on East Asia. Semiconductor shortages crippled automotive and electronics sectors. Red Sea diversions forced reroutes that added $200 to $400 per TEU in incremental costs. Sanctions on Russian oil and gas disrupted energy inputs for manufacturing across Europe. Geopolitical risks can disrupt global supply chains and increase costs at a speed that exposes every unhedged dependency.

Supply chain resilience is now as important as cost optimization. Organizations are moving away from single-source dependencies in supply chains and toward diversified, multi-corridor architectures. Three concepts are reshaping manufacturing footprints:

- Friendshoring: favoring suppliers in politically aligned or stable jurisdictions to mitigate risks from sanctions or conflict.

- Nearshoring: moving production closer to end-markets to reduce transport risk and shorten lead times.

- China-plus-one: maintaining Chinese suppliers while adding capacity in India, Southeast Asia, the Middle East, or Eastern Europe.

Companies are diversifying suppliers across multiple countries. Strategic competition forces firms to rethink technology supply chains, particularly in semiconductors and critical minerals. Sanctions can lead to supply shortages of essential raw materials, as the Russia-Ukraine conflict demonstrated with fertilizer and metals. Effective risk management strategies include supply chain diversification as a structural principle, not a crisis response. Resource nationalism in several countries further complicates access to inputs, making geographic spread essential.

The trade-off is real: resilience increases costs, duplicates overhead, and adds regulatory complexity. But unpriced geopolitical exposure destroys entire markets when crises hit. The money saved on lean, single-source supply chains evaporates when a chokepoint closes.

Sector and geography: building a resilient business portfolio

Boards must think in portfolio terms across both sectors and regions. Geopolitical risks can cause significant fluctuations in financial markets, and a portfolio concentrated in a single political bloc or sector is a leveraged bet against stability.

A geographically resilient portfolio looks like this:

- Diversified footprints across stable OECD markets and emerging hubs in the GCC, ASEAN, and Africa, balanced across different political blocs so that sanctions or trade wars do not hit the entire book.

- Sectoral diversification combining long-cycle assets (infrastructure, energy, logistics) anchored by sovereign policy with shorter-cycle digital, service, and tourism assets that offer flexibility.

- Middle East economic clusters as hedges: a supply chain base in Saudi Arabia or UAE can serve Africa and South Asia when other corridors are under strain. Destination marketing and cultural investment in the GCC are hard assets partially immune to commodity-price cycles.

- Explicit exit pathways pre-planned before crises emerge. Predetermined triggers, such as political violence indices, sanctions threat levels, or regulatory divergence thresholds, help organizations avoid paralysis when economic conditions deteriorate.

Increased scrutiny on cybersecurity is linked to geopolitical tensions, and cyber attacks on critical infrastructure can cascade across portfolios. This makes digital resilience another dimension of geographic risk, not a standalone IT concern. Investors increasingly demand stress testing and scenario planning as proof of portfolio robustness.

Risk intelligence as a standing business function

Successful geopolitics in business depends on building permanent risk intelligence capabilities.

Geopolitics as a business function means permanent capability, not ad hoc memos during crises. Continuous monitoring identifies early warning indicators of risk. Organizations must continuously monitor geopolitical developments to remain agile, and that requires a dedicated team, structured feeds, and integration into decision-making processes.

What this capability looks like inside a large organization:

- A central geopolitical risk unit reporting into strategy and finance, not buried in compliance or security.

- Embedded analysts in procurement, treasury, legal, and marketing who understand how to translate emerging threats into operational response.

- Structured feeds including horizon scanning, regulatory watch, sanctions monitoring, and social unrest tracking integrated into executive dashboards. Manual processes for tracking political shifts are insufficient at scale; automated monitoring and external advisory partnerships are crucial.

- For Saudi and GCC institutions, this function must bridge global developments with local policy agendas and Vision 2030 programs. What sanctions between major powers mean for Saudi trade routes or what geopolitical risk indices reaching levels comparable to the start of the Russia-Ukraine conflict mean for procurement timelines must be translated into local context.

Clients of advisory firms increasingly expect this intelligence to be integrated, not siloed. To stay informed requires discipline, not just access to data.

Implications for marketing, brand, and stakeholder engagement

Geopolitical risk does not stop at the treasury. It reaches brand positioning, campaign calendars, sponsorship choices, and stakeholder engagement. In sectors like banking, media, sports, culture, and tourism, a misread of political context can trigger reputational damage faster than any financial loss.

Destination marketing and nation-branding in Saudi Arabia and the GCC are intertwined with political positioning and regional competition. The tourism push toward 2030, major sporting events, and cultural initiatives like Diriyah are exercises in soft power as much as economic development. How the region communicates itself abroad directly impacts investor confidence, brand equity, and demand for services across the global economy.

Social unrest, conflict, or sanctions can force rapid repositioning of campaigns, content, and event calendars. A sponsorship tied to an event in a sanctioned jurisdiction carries legal and reputational risk. Digital content may face scrutiny. Partnership choices must account for the political optics of alignment. Cross-sector thinking helps here: patterns from finance, sports, and culture allow organizations to anticipate public and stakeholder reactions to geopolitical shocks, applying solutions from one sector to challenges in another.

Marketing, communications, and brand leadership should be part of the geopolitical conversation at the executive level, not informed after the fact. The economic impact of reputational misalignment can rival direct financial losses.

How executive teams should operationalize geopolitical insight

Operationalization requires governance, not good intentions. Boards should assign explicit responsibility for geopolitical oversight. In 2023, GCC countries attracted $47 billion in foreign direct investment, with Saudi Arabia accounting for 62 percent. Capturing that kind of capital flow requires institutions that understand geopolitical positioning as a competitive advantage.

Specific governance moves:

- Link geopolitical scenarios to financial stress tests and tie regional exposure to risk appetite statements.

- Connect geopolitical analysis to investment committee papers, market entry approvals, and major procurement decisions. No capital above a threshold should deploy without a political risk assessment.

- Hold regular cross-functional sessions bringing together strategy, finance, operations, supply chain, and communications to review the geopolitical picture.

- Use effective strategies drawn from Saudi and GCC case studies where integrated approaches have either prevented losses or enabled faster moves into emerging opportunities.

These are not theoretical recommendations. They are the operating architecture that allows organizations to rely on structured intelligence rather than reactive scrambling.

The Middle East’s evolving role: from perceived risk to strategic anchor

The Middle East, and especially the GCC, was historically viewed through a risk lens: conflict, instability, uncertainty. That frame is outdated. Energy transition investment, sovereign wealth fund activity, and major sports, culture, and tourism initiatives position the region as a long-term economic center, not a peripheral risk zone.

GCC sovereign wealth funds are active globally, deploying record capital into AI, digital infrastructure, and technology platforms. Organizations can leverage Riyadh and other GCC cities as bases for resilient regional supply chains covering Africa, South Asia, and parts of Europe. The infrastructure being built, from ports and airports to financial districts and digital zones, creates corridors that reduce dependency on vulnerable routes.

The balance matters. The region still faces tensions, and risk management remains vital. But the direction of travel is toward greater institutional capacity, regulatory depth, and economic diversification. The risk per investment dollar is falling. For organizations that understand this trajectory, the Middle East is becoming an anchor, not an exposure.

Strategy in an age of moving borders

Geopolitics has become a standing business function, essential to corporate strategy, supply chains, market entry, and brand positioning. The evidence from the past decade is unambiguous: businesses that treat political risk as peripheral will find themselves excluded from the markets that matter most and exposed in the markets where they remain.

For institutions operating in or from Saudi Arabia and the GCC, the stakes are compounded by the region’s central role in new global economic clusters. Ignoring geopolitical risk is not an option when the region is simultaneously exposed to global shocks and generating its own gravitational pull on capital, talent, and technology. The future belongs to executives who build geographically and sectorally resilient portfolios, capturing upside as new hubs rise while managing exposure as old structures fragment.

Ultimately, geopolitics in business is no longer optional for organizations operating across borders.

Shifting alliances, emerging markets, and regional programs like Vision 2030 will keep redrawing the map through 2030 and beyond. No single adjustment will be sufficient. The organizations that thrive will be those that treat map-reading as a continuous discipline: structured, funded, embedded in governance, and connected to every function from finance to marketing. The map will keep moving. Strategic adaptation is not a project with an end date. It is the operating condition of this decade.Organizations that master geopolitics in business will outperform those that continue treating it as a secondary concern.